The Future Of Print Media – Capstone Report 2011

Samantha Barthelemy

Matthew Bethell

Tim Christiansen

Adrienne Jarsvall

Katerina Koinis

Advisors: Anya Schiffrin, Columbia University

Martha Stone, World Newsmedia Research Group

Abstract: Many commentators and analysts have confidently declared that the age of the printed newspaper is over. Industry wide developments including falling advertising revenues and fragmented audiences that are increasingly shifting online are said to signal the end of the newspaper industry as we have come know it. This paper seeks to establish to what extent this characterization of the newspaper industry’s decline is accurate through an in-depth literature review, a series of lectures by experts in the field, and by conducting 24 interviews with publishers and editors from six countries. The study finds that while there are clearly significant shifts taking place within the print industry, particularly around attempts to monetize online content and find alternative sources of revenue to replace falling advertising revenues from print, the decline of the industry is overstated. News organizations are going through a process of transition and adaptation. In addition, the paper shows that the narrative of newspapers being in perpetual decline is mostly Western centric, and does not take into account regional variations and the fact that in many emerging countries, print newspaper sales are robust and growing.

TABLE OF CONTENTS

04…..INTRODUCTION

07…..METHODOLOGY

10…..POLICY RELEVANCE AND IMPLICATIONS

12…..TWIN CRISES OVERVIEW

17…..ALTERNATIVE REVENUES

26…..ONLINE MONETIZATION

34…..REGIONAL VARIATIONS

42…..CONCLUSION

44…..APPENDICES

45…..BIBLIOGRAPHY

The Future of Print Media – INTRODUCTION

At the 2010 International Newsroom Summit in London, Arthur Sulzberger, Jr. The New York Times editor said, “We will stop printing the New York Times sometime in the future, date TBD.” This admission by the editor of one of the leading newspapers in the world was only a small part of the widely held debate in the news media industry on the “death of print”(1).

This paper examines the validity of the claim that the era of newspapers having a business model based around print is over. The traditional business model, where journalists would write stories, submit them on deadline for copy editing and then the resulting content would be sent to the printing press, is said by many to be redundant in an age of fragmented audiences, high speed internet and mobile devices. By gaining an in-depth view of the current media landscape across the globe we have sought to evaluate these assertions, that at times can develop into hyperbole. At the heart of the research are interviews with newspaper publishers and editors from around the world to find out their assessment of the current media climate, as well as their papers’ strategies for future growth.

Our client for this research is the World Newsmedia Research Group (WNRG), a global, not-for-profit research association. It is a subset of the World Newsmedia Network, a notfor-profit multiple media association devoted to advocacy on the media industry’s key issues around the world. WNRG’s mission is to provide media owners with actionable, strategic research for their businesses in TV/video, radio/audio, newspaper, magazine, mobile, Internet, e-reader and any future channels. WNRG produces two significant annual research projects: The World Newsmedia Innovation Study, and the World Newsmedia Digital Revenue & Usage Trends Yearbook. This Capstone used the knowledge acquired throughout the semester and interviews conducted to provide WNRG with case studies to be included in their upcoming World Newsmedia Innovation Study.

The central questions we sought to answer are whether the alleged death of print is a global phenomenon and what strategies individual print media organizations are pursuing to continue operating. The conversations often, albeit not always, developed into a discussion on the Internet, online media and the big question about how to get the traditionally free provision of online news content to be profitable. This challenge preoccupies editors and executive across the globe, though not with the same degree of urgency. From the information gathered, can we conclude that we are witnessing the death of print? The answer is no, at least not globally. The pessimistic narrative of print’s decline has mainly been driven by Western economies – the United States, the United Kingdom and central Europe – that have experienced dramatic reductions in print newspapers’ major revenue streams: advertising and print sales. Indeed this paper will show that we are witnessing not the “death” of print but rather the adaptation of print and news organizations to rapidly changing consumer patterns and a corresponding shift toward digital content, exacerbated by the recent financial crisis. The core of this research highlights various business strategies to maintain sustainable revenue streams in print, online and through alternative media channels.

Initially, we outline the research methodology used to gain in-depth knowledge of the state of print media today and the external variables affecting it. We examined current academic findings, conducted interviews with editors and executive of print news organizations across the globe and conversed with experts and industry insiders. We highlight the policy relevance of an independent and diverse media realm and what challenges current developments pose to free media. We then provide a snapshot of recent developments that have led to the “doomsday mood” among some industry professionals, what we name the “twin crises.” Focusing on our findings we present new and adapted business models from regional consolidation of print business into one organization, to broadening the model to include alternative revenue streams and, importantly, the challenge to monetize online news.

Finally, it is important to note that the newspaper industry has been in the process of adaptation to a new technological era for longer than many commentators and analysts have acknowledged. The changing news environment is not a new phenomenon brought about by the Internet alone. This paper seeks to place the most recent challenges to the traditional business model in context, and establish where the industry is moving in the medium term. By supplementing analysis of literature and commentary with interviews with those best placed to discuss industry trends and developments, we were able to gain a more accurate sense of the future of print media.

The Future of Print Media – METHODOLOGY

The goal of our study was to detect and evaluate business trends in the newspaper industry worldwide. We interviewed leading publishers and editors in over six countries across the globe and supported our findings with additional research and analysis. Given the unparalleled speed at which the media realm has been changing in the past ten years, this research project, like any other, is only going to provide a snapshot of the state of the industry. By talking to editors and publishers, our objective was to find out how the newspaper industry is coping with changes brought on by the “twin crises;” the transition from a traditional print business model and the increasing impact of the internet. We sought to achieve this objective by identifying our market, researching market trends both in the print and digital realm, and engaging with decision makers, academics and practitioners. Our topic guide for interviews was focused on the present and the future of print newspapers and media organizations’ business strategies. We sought to find out not only what participants’ current strategies were, but also how they intended to adapt to trends in the next three to five years. We put together our topic guide while we gathered and analyzed current research and literature, enabling us to better probe our participants as to their predictions around the future, industry trends and how they relate to their publication. We did so by broadly focusing on the following topics:

- The most important strategies for their respective print paper(s) going forward;

- Discussing these (and in some instances additional) strategies in the context of the twin crises;

- Exploring the subject’s attitudes toward existing alternative strategies we encountered throughout our research.

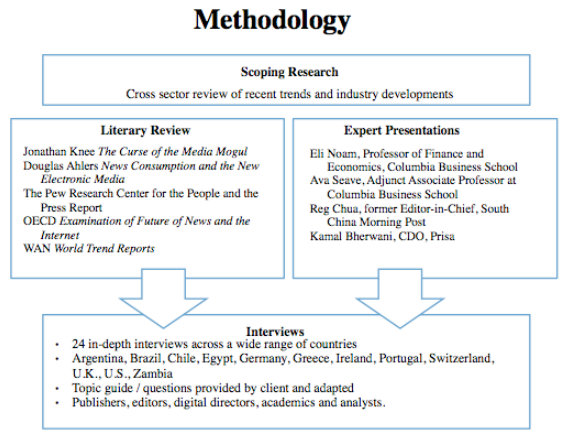

Our conversations rested on two pillars: an in-depth literary review, as well as drawing on the knowledge of experts from the academic and professional realms. Experts included Eli Noam, Professor of Finance and Economics at Columbia Business School, Reg Chua former Editor-in-Chief of the South China Morning Post, Kamal Beherwanti, CDO of the Spanish Media Conglomerate PRISA and Ava Seave, Adjunct Associate Professor at Columbia Business School.

Figure 1 – WNIS Methodology

In the second phase of our research process we conducted interviews with representatives of major media companies and newspapers in the countries selected for the study – Brazil, Chile, Germany, Greece, Switzerland and the United Kingdom. The World Association of Newspapers (WAN), Pew Research Centre for the People and the Press, the Organization for Economic Development among others served as important sources. The 24 in-depth interviews focused on business strategies of the organizations, with questions focusing on the single most important strategies the organization is pursuing in 2011, the three most important business projects for the respective newspapers for the coming two to three years, and growth potential. Areas discussed included both reporting and journalism, business strategies of print newspapers and issues related to the monetization of online content. Though subjects were reluctant to discuss detailed strategies, we were able to detect universal and regional trends and the interviews were supplemented with relevant up to date market data.

The Future of Print Media – POLICY RELEVANCE AND IMPLICATIONS

Vibrant and robust media is a critical part of a functioning democracy. It keeps the public informed and allows people to engage in lively debate. Citizens depend on the media for information, a tool with which they can engage in informed discussion and hold political leaders accountable. The media provides a “marketplace for ideas” that “scrutinizes arguments and forces ideas to confront each other in common forums,”(2) and is unquestionably a cornerstone of a successful representative democratic system. This has become more pronounced in the past months as citizens from Tunisia to Libya took to the streets to demand freedom from oppression. While it is new, social media’s role is being hailed as having carried information across boundaries, informed and thus supported the revolutions. However newspapers, their reporting, analysis and commentary, played the leading role in providing in depth analysis of these major international events. This applies to mature readers and youth in equal measure “who are just as interested and just as concerned about these events as their parents,” according to Dr. Aralynn McMane, Executive Director of Young Readership Development at WANIFRA.

The rapidly changing media environment to which newspapers have had to adapt forced many to rethink traditional news-making. In addition, publishers and editors are considering questions around the way in which news is consumed and whether alternative revenue streams ought to complement the traditional news-making model. In the United States, newspaper circulation dropped an average of 8.7 percent between 2007 and 2009. Although it has since slowed to 5 percent, according to the U.S. Audit Bureau of Circulations, the industry is far from being “out of the woods.” As a result of this instability, media ownership threatens the diversity of voices and viewpoints. However there is a significant amount of variation in industry trends. Markets in Europe and the United States face significant pressures due to declining readership and losses in advertising revenues.

In the United Kingdom circulation fell by 25 percent between 2007-09, second only to the US, where the decline was 30 percent. Greece saw a decline of 20 percent, Italy of 18 percent and Canada of 17 percent (3). Conversely, newspapers in much of the developing world have been experiencing growth; circulation increased by up to 30 percent in Africa, 13 percent in Asia and 4.55 percent in South America. On the African continent, newspapers suffer from a lack of advertising revenue and investment in new technology and personnel (4). However the common aspect to all countries is the speed at which the industry is changing, and the common challenge consequently becomes trying to keep up.

The Future of Print Media – OVERVIEW OF THE “TWIN CRISES”

The newspaper industry is facing two simultaneous crises stemming from the decline in newspapers’ circulation and advertising revenues and the rise of widely available and free online news content. The United States suffered the most severe fall in circulation, and advertising revenues dropped 8.7 percent in the period from March to October 2010. This reduction in revenues from advertising was further exacerbated by the financial crisis of 2007-08 (5). The entrance of alternative online sources of news also marked a new era of digital competition. Consequently, one of the principal challenges for news organizations became the establishment of new, alternative revenue streams that do not rely solely on the traditional print model.

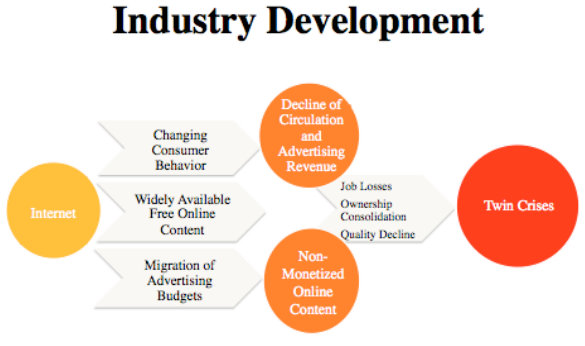

Figure 2 – WNIS Industry Development

Figure 2 points to three important factors that contributed to the “twin crises.” Print circulation has been declining for decades, but consumer behavior began to change most rapidly with the increasing use of the Internet (see Figure 2). The breadth of information available online, and the opportunity to personalize news consumption according to individual interests, coupled with being able to get news updates several times a day – as opposed to once in the morning over coffee – pushed audiences online for their news.

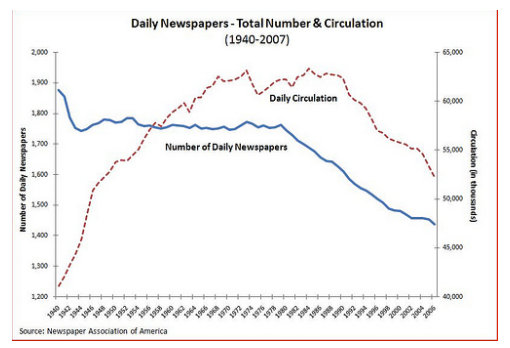

Figure 3 provides a clearer idea of how steep the decline in circulation for American daily newspapers has been in the past decades.

Figure 3 – Daily US Newspapers 1940-2007

A second critical factor is the fact that the majority of online content is available for free. The sources are innumerable; from opinion blogs to online only newspapers, such as The Daily, a newly launched newspaper customized for Apple’s iPad users. News information websites and applications continue to grow exponentially. The idea of getting news for free online became even more appealing during the financial crisis of 2007-8, a period when newspaper circulation in the United States dropped 30 percent (6).

Thirdly, changes in consumer behavior were accompanied by the migration of advertising budgets from the print to the online realm, albeit at a fraction of the revenues provided from print advertising sales. Scott Karp, co-founder & CEO of Publish2, a content distribution platform, refers to this phenomenon as the 10 percent problem. Taking The New York Times as an example (prior to the paywall introduced in March 2011), Karp points out that print circulation is about 10 percent of total audience reach, while online advertising revenue is about 10 percent. The result is a nearly “perfect inverse relationship” of what online revenues and print advertising should generate given their respective readership (7).

The combination of these three factors, and their consequences, have led to what we now know as the “twin crises.” News organizations today are faced with one complex, central challenge: dealing with declines in print circulation and advertising revenues, while facing and competing with increasingly available non-monetized online content. The “twin crises” have a range of consequences for the industry. First, job losses continue to occur and older, more experienced, journalists that cost more to retain, are becoming easily dispensable. Second, we have witnessed a decline in journalistic quality and the rise of “down-market” or popular publications. It is interesting to point out that the growing commercial success of tabloids (8) has been linked to the broadening of the reading public and the inclusion of new, lower-income audiences. Finally, news organizations are turning to more competitive and qualitative approaches – as in the cases of paywall launching and further ownership consolidation, with mega industry players acquiring smaller ones. However it should be noted that even during this global economic downturn, newspaper circulation worldwide fell only slightly (9).

If we take into account countries like Germany, Austria and Brazil, it is evident that publications are thriving. Newspapers’ circulation in Brazil has grown steadily since 2004, reaching a record high of 72.5 copies sold daily per 1,000 adults in 2008 (10). German and Austrian markets have shown strength compared to other Western markets. In fact, hardly any other market in the world generates higher incomes from advertising and sales than the German press (11). Similarly, the Austrian newspaper market was hardly hit by the financial crisis; circulation decreased by only 2 percent from 2007 to 2009.

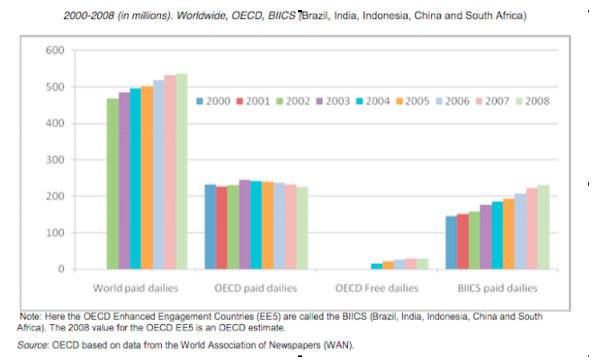

Figure 4 presents an overview of paid-for daily newspapers’ average total daily circulation worldwide, from 2000 to 2008:

Figure 4

Efforts to close some publications’ content behind a paywall, limiting it to a targeted audience that would be willing to pay a premium have not always succeeded. Major publications such as The New York Times and the Greek newspaper Naftemporiki have proceeded to placing their online content behind a paywall.

However, there is no assurance that by imposing a fixed charge on their services, audiences will follow and companies will generate desirable revenues. It would take a niche market to value a rare and specialized product in order to allow for paid-for content. For instance, the Wall Street Journal and the Financial Times produce in depth analysis, feature reports and commentary by experts and public intellectuals, targeting a niche audience of business people who are willing to pay a premium for this unique information. This content is difficult to find free online, and under these circumstances interested readers do pay for content (12). Nevertheless, successful cases of publications charging for their online content are still the exception, as the vast majority of online material is still widely available for free. A full discussion of the issues around online monetization can be found in the next section. The decline in circulation in some countries resulted in further declines in advertising revenues. Publications have tried to find ways to make up for the loss of print editions through alternative investments, either in the media or other unrelated fields (13), or through the monetization of online content – which, as mentioned, is not always easy or successful. The following section provides further details on the approaches to generating revenues from alternative, non-print newspapers, sources.

The Future of Print Media – REVENUE ALTERNATIVES

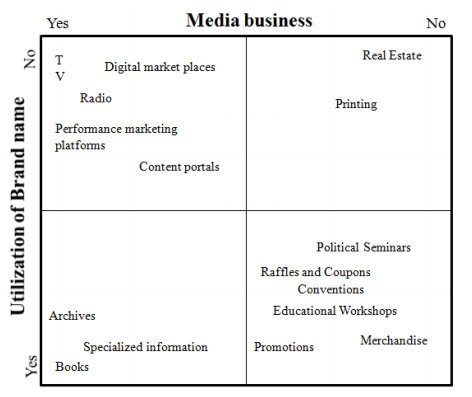

As a result of changes in consumer behavior and declines in revenues from advertising, newspaper-publishing companies, particularly in developed Western economies, are looking for alternative sources of revenue. Even in emerging markets like Brazil, where newspapers’ circulation grew by 25 percent in the last five years (14) and advertising revenues are still increasing, companies are seeking to decrease their strong dependence on print. To deal with this challenge, news organizations are diversifying their business strategies and moving beyond news aggregation and distribution; primarily seeking to invest in other media and non-media businesses and strengthen newspapers’ brand names (see Figure 5). The following section uses “branding” and “business type” to differentiate between the sources of alternative revenue streams.

Figure 5: Alternative Revenue Products

The “Brand Effect”

There are various strategies to increase alternative revenue streams by making use of the newspapers’ brand name, or using the “Brand Effect”. The idea behind the brand effect is that newspapers develop significant brand loyalty from their readers and often come to be associated with certain attributes; reliability being a central one. An example of the brand effect is the creation of “brand families” to carry on the newspaper’s name to new products (15). There are two general ideas behind newspaper companies’ efforts to stretch the use of their brands: “brand extension” and “customer identification.” The business model of a newspaper is to assemble information, place it in context and provide readers with in-depth analysis. Finding new ways to present and “sell” information using an already established brand is an alternative revenue stream being pursued by publications we spoke with. The idea of “brand extension” is similar to “product-line extension,” defined as the appearance of another product that a company introduces within the same market after its existing product. Newspapers are in the information market and their major products are news and information. The brand value is an expression of the trustworthiness readers feel toward the newspaper or the experience of customers regarding the quality of its information. Some newspaper companies, including Germany’s Frankfurter Allgemeine Zeitung, offer huge online archives with powerful search engines behind a paywall. The information is presented in a differentiated, more detailed way than on its newspaper. Niche consumers, who seek specific information, like an academic or a financial analyst, may be more willing to subscribe than a private consumer who wants simple news updates. Many other newspapers offer specialized information with regards to, among other areas, career search, education, health, real estate and cars. They offer this information through special theme portals, in a more detailed manner than is presented in their regular publications. The Chilean newspaper, El Mercurio, is currently setting up a second website which is entirely behind a paywall. The content is specialized and targeted to financiers, lawyers and other professionals with a specific need for niche analysis and information.

The information is still the main product, but it is presented and offered in different ways to attract new customers and to make old customers start paying, or spend even more for the brand they are accustomed to. Another way of extending the newspapers’ brand is to use its name on other product labels (ie, books or wine), adding value to that specific product since it is linked to an already established and trusted brand. Newspapers can offer their expertise in certain areas, including book reviews and food sections, and participate in creating revenue streams for book publishers or wineries based on their recommendations. Süddeutsche Zeitung, a German national daily newspaper, created the “SZ Edition” with famous books and movies that do not belong to the Blockbuster segment. Every month Süddeutsche Zeitung recommends news books and movies; customers can subscribe for the entire year or buy them separately through the newspaper’s website. The American newspaper, Financial Times, and the British The Guardian, use a similar model to sell reviewed books. The concept also seems to work well for The New York Times, which has an entire online store. It also has a food section with a high reputation, and uses it to generate additional revenue streams by selling wine from exclusive wineries outside the United States. In 2010, the Brazilian newspaper A Gazeta, owned by Rede Gazeta, launched a guide of medical specialties, “a better quality catalog than the yellow pages,” according to Director General Carlos Fernando Monteiro Lindenberg Neto. This has been an exceptionally important source of revenue for A Gazeta, as over 20 percent of revenues from print products come from the publicity embedded in these publications (16). The second general approach of newspaper companies to make use of their brand is not directly related to the media business. Companies organize interaction among people in the form of seminars, conventions, debates and workshops. This approach makes use of newspapers’ human capital and journalistic expertise to sell information and train individuals. Among many examples are: Greece’s Naftemporiki, which holds a 35 percent share in a company that organizes medical conventions; HSM Education, a São Paulo based partnership of Grupo RBS and BR Investments, which offers executive training, editing courses and consultancy, and; Brazil’s media conglomerate Rede Gazeta, which promotes educational events and seminars debating political issues.

There are also approaches that are not related to the media business, which use the brand but not the human capital or expertise of newspaper companies. Organizations try to use the brand loyalty established with their customers, in combination with their brand image, to sell merchandise. Switzerland’s Neue Züricher Zeitung sells bicycle bags and The New York Times has an entire webstore selling, among other products, coffee mugs and pencils; many German newspapers also sell watches. Some Brazilian publications, including Noticia Agora, invest in embedding coupons, raffles and other promotions in their online and print product. Even though this section presents different ways through which news companies can diversify their revenue streams and generate new sources of revenue, there is no silver bullet to make up for the steep declines in advertising revenues.

Using and Acquiring Assets other than the Brand

There are two business models of strategic importance that do not use directly newspapers’ brand name. The first approach is to acquire or create new assets, including websites, TV stations, or radio stations. The second approach is to use existing assets more efficiently.

The first model is specifically related to digitization. On the one hand the digitization of media has become a major problem for print newspapers, but on the other hand it offers important revenue potential and is an investment area of strategic importance for media companies. According to Christoph Keese, President of Public Affairs of Germany’s Axel Springer AG, the German digital sector has three distribution channels, which are (21) important for newspapers: Internet, TV, and radio. Many newspaper companies around the world are invested in all three realms. For example, Grupo RBS, one of the leading media groups in Brazil, headquartered in the southern city of Porto Alegre, owns 18 TV stations, two community TV stations, one rural channel, 25 radio stations, eight newspapers, four Internet portals and other media businesses.

There are three generic models on how to monetize (charge for) online content:

- The first model is based on subscriptions. The customer consumes certain content for a certain period of time -yearly, monthly, weekly or daily – after paying for access to the content behind a paywall. This model is also called “market places.” Many newspaper companies, like The Guardian or Axel Springer AG, started online-dating websites (parship.de) or job search (stepstone.com) websites.

- Another model is based on commissions. The commission has to be paid, if an intermediation between a customer and the supplier takes place. The newspaper company offers a “performance-based marketing platform,” which can be subsumed under “ecommerce.” The website gets a fixed amount or a percentage of the revenue of the arranged business from the provider of the goods and services offered on the website. A very successful example for such a market place in Germany is Springer’s myhammer.de, where craftsmen can offer their services.

- The third and most important model is based on advertising revenues. In 2011, the global market for Internet advertising was projected to reach U$71 billion (17). Idate, a consulting group specialized in media, estimated an average growth for online advertising of 15.5 percent between 2010 to 2012; the total advertising market is predicted to increase by only 4 percent during the same period (18).

The idea of online advertising is similar to that of print advertising. Websites offer space where their advertisers can put their ads to inform potential customers about their products (19). However the Internet offers many advantages in comparison to newspapers, because Google’s technologies, e.g. adsense and adword, make it possible to tailor ads for specific customers and for specific regions of the world. It becomes easier to target specific customers online, and advertisers can reasonably expect their ads to be more effective (20). Newspaper companies can generate revenue streams from online advertising by creating “content portals;” for example Greece’s IMAKO Group offers a travel website. The customers, in this case Greek hotels, can place their ads specifically next to the search results of the customer who uses the IMAKO Group’s website to book a holiday trip in Greece (21).

Another interesting approach to increase revenues from online advertising is to create social networks with a distinct local audience, making it easier for advertisers to target customers interested in local products. For instance, Germany’s Neue Osnabrücker Zeitung offers a Facebook-like website for people in its circulation area. This is highly attractive to smaller local advertisers because the audience is very distinct and they can tailor their ads to people in this region. This results in more effective advertising campaigns (22).

Television is the second major digital channel newspaper companies invest in. Many newspaper companies started to invest in TV in the last decade to acquire expertise regarding news production and access to its advertising revenues. For example, PRISA, the leading Spanish media company, acquired 95 percent of the leading Spanish TV company, Sogecable, in 2008 and became a major player the Spanish pay and free-toview TV market. The budgets for TV advertising are much bigger than those for other types of media, making TV a very attractive alternative source of revenue for newspapers.

Ioannis Liotos, Commercial Director of Greece’s Naftemporiki, says, “Many businesses have turned to television, even more so since TV stations decreased their prices in advertising thus making them a lot more competitive.” Global revenue streams from TV advertising are expected to reach U$169 billion, 35.5 percent of the global advertising market in 2011 (23). Revenue streams from TV advertising are predicted to increase by 3 percent per year on average in the period from 2010 to 2012; this is lower than the 4 percent increase expected for the total advertising market for the same period (24). These numbers seem low in contrast to the growth of online advertising revenues of 15.5 percent. However it is important to note that TV advertising is a mature market, which, in 2011, is 2.5 times the market for Internet advertising. For instance, Brazil is one of the ten largest advertising markets in the world, with expenditure highly concentrated in broadcast television – in the last decade TV networks have absorbed 59 percent of all advertising revenues in the country while other traditional media such as newspapers, magazines and radios, had their share reduced, generating significant constraints for their future growth. The country is a clear example where broadcast television remains the dominant medium – contrary to trends in parts of the post industrial world. Data from the National Association of Newspapers show that in 2009, 14.1 percent of advertising investment went to newspapers (60.9 percent to television) compared with 21.7 percent in 2001 (57.8 percent to television)(25). Under thisscenario, many newspaper companies are being pushed to increase their scope, seeking to become media conglomerates and attempting to access other, non-print, advertising markets. The main problem with merging newspaper companies and TV stations is regulation. Cartel authorities have to prevent the abuse of market power accumulated within single companies.

This is a particularly sensitive issue for news companies in established democracies. The news industry is regarded as the “fourth estate” and therefore it has to be supervised very carefully. The investment in TV stations has to be differentiated from the investment in TV content production companies. The business of the latter is very diverse and covers everything from entertainment, e.g. TV shows and daily soaps, to news. Less problematic is the investment in TV content production companies, if they focus on content for entertainment and not news. The cross ownership of newspaper companies and TV stations can become problematic if the merged company has a significant share of the news market. This critical level of market share has to be defined by the cartel authorities. For instance, Springer in Germany could keep its shares of its TV content production company Schwartzkopf, but it had to sell its shares of the TV station Pro7-Sat, a private TV station in Germany, in 2006 (26). In contrast, the takeover of Sogecable by PRISA was approved by the Spanish stock market regulator CNMV, because PRISA only has minority stakes in the top free-to-air TV operators in Spain.

The third distribution channel is radio, for which the major source of revenue is also advertising (27). In 2011 the global radio advertising budget is expected to reach U$30 billion, or 6.5 percent of total global expenditures on advertising. In the period between 2010 and 2012 global advertising revenues are predicted to grow at a rate of only 1.9 percent. Radio stations have suffered in recent years, especially in the United States, the most important radio market in the world with 50 percent global market share for advertising (28). It has become increasingly difficult for radio stations to gather listeners for advertising-based radio programming because of the rise in online information bases (29). In contrast to the small growth rate of radio advertising predicted for 2012, online advertising is expected to increase by 15.5 percent in the 2010 to 2012 period (30).

The second approach to generate alternative revenue streams, while not making direct use of newspapers’ brand name, is to use existing assets more efficiently. Newspapers with big printing capacities, like Greece’s Naftemporiki, can offer competitors with smaller circulation to do the printing in their printing facilities. Printing and distribution are no competitive edges of newspaper companies. Hence, this scenario is a win-win situation, decreasing costs for all participants. The idea is that larger capacities realize economies of scale. This might even lead to mergers of printing facilities like Prinovis, a joint venture of Germany’s Bertelsmann Arvato and the publishing companies Axel Springer and Gruner & Jahr. (26)

The Future of Print Media – ONLINE MONETIZATION

As discussed above, a consistent theme across our interviews included the strategies and approaches to monetizing online content. In the context of our discussions, this generally referred to the challenge of charging for content produced by the publication – and offered online – that traditionally would have been charged for in print form. As noted, the fragmentation of the newspaper industry and the financial challenges facing publications have not been caused, but exacerbated, by the rise of the Internet. In fact, the traditional print model has been under threat for years. However having to face increased competition from online news providers and aggregators, like The Huffington Post, Yahoo News, Google and countless others that are able to publish content for free, newspapers have lost their monopoly on information dissemination. Like all the other players in the industry, newspaper publishers are being forced to scramble for ways to remain profitable as new media continues to develop rapidly. All of those who participated in our interviews and conversations were greatly concerned with, and had evidently been spending a significant amount of time thinking about, how to monetize their online output. For Liam Kavvanagh, Managing Director at the Irish Times, the most important thing is to protect and maintain print operations, while at the same time developing and accelerating online activities and trying to develop and accelerate significant and meaningful online revenues.

The following sections outline our main findings from the literature review, research and interviews on the approach to charging for online content in the form of paywalls and the use of social media, mobile platforms and applications to increase newspapers’ online audiences.

Paywalls

The big question of how to make money from online content could of course be answered very simply: by charging for it and putting in place a “paywall.” Content that is behind a (27) paywall is only accessible to the online user if they provide credit card details and subscribe to the publication online; a “pay to play” model of providing digital content. There are numerous examples of publications that have had a strict paywall in place for a considerable amount of time; they are mostly niche publications like the Wall Street Journal or the Financial Times. These publications’ content is at a premium for the detailed and unique analysis they provide, the speed at which they are able to provide it, or both. As is the case with the WSJ and the FT, this is generally financial or business news; unlike the mainstream newspapers that cover news from across a range of industries, perspectives and subject areas. As a result, less “specialized” publications are dealing with a delicate balance. “For the vast majority of people who read a news site, the price they’re willing to pay is zero. For a few, it’s something more. The key question […] of any paywall […] is how to maximize the revenue generated from those two extremes and the various gradations in between” (31).

While conducting our research we detected a sense from a number of interviewees that there was an ambivalence about making the leap into charging for content. In the words of Carlos Fernando Monteiro Lindenberg Neto, General Director of Brazil’s Rede Gazeta, “We do not want to be the first ones to take the unsympathetic decision of charging for content that is widely available for free.” However interviewees also demonstrated an appreciation that there would be a period within the next 2 to 3 years when the industry would settle on “a model that works.” To be sure, our interviews indicated that the industry is moving towards a consensus that however the challenge is approached journalism cannot be free of cost; high-quality contents need a price label. The question then becomes what should that price label look like and how should it function?

Some of the most significant stories in the last year at The Guardian have emerged as a result one way or another of social media (32). Therefore, it makes editorial sense to continue to expand the openness and interactivity of content.

But in more linear products like closed applications or videos where there is less potential for collaboration, Steve Folwell, Head of Strategy at the Guardian Media Group says, “We have absolutely no journalistic or editorial objection as far as I understand with being paid, we’ve been being paid since 1821 in print.” Therefore, it becomes a case not about whether publications charge for content, but about what they charge for and how.

In previous sections, we have established that publications are currently pursuing a range of approaches to dealing with the question of whether, and how, to charge for online content. It is important to note that a key finding of our research and interviews is that there is not one dominant model of monetizing online content. Most publications are currently supplementing existing approaches by investing additional resources in social media and the development of mobile applications. The news industry appears to be in a state of flux as to which model is seen as the most likely to deliver the necessary revenue to compensate from the loss of revenue from print advertising sales:

- Full Paywall – As put in place recently by The Times of London, this model would demand a full subscription to access any online content;

- Pay for Premium – The prime example of paying for premium content would be the Wall Street Journal, where the primarily business focused news is available for a cost, but a limited amount of generic news is available for free.

- Hybrid – The New York Times is the prime example of a hybrid model, where the paywall only becomes effective when you have accessed your complimentary 20 articles. After this point you are required to subscribe, or read only articles you are directed to via social networking or online searches.

- Free Content – Many publications, for instance The Guardian, are relying on providing content for free, increasing audience size and therefore their advertising revenues.

In addition to the models briefly outlined above, a number of publications discussed the use of increased levels of advertising more narrowly targeted to users own interests; as noted in the “Alternative Revenues” section, using newspapers’ brand to move into ecommerce or as one interviewee described it, the area of “transaction.”

Social Media

The increasing importance of social media and its impact on the “traditional” journalistic process was another key theme to emerge from our interviews. While in itself social media does not provide immediate opportunities for increasing revenues, it provides publications with ways of producing more accurate content more quickly, and of being able to increase the audience for content. A widely used definition of social media is provided by Andreas Kaplan, “A group of Internet-based applications that build on the ideological and technological foundations of the Web 2.0, which allows the creation and exchange of user-generated content” (33). Invariably, in our interviews, the social media discussed was around the social networking site Facebook, the micro-blogging tool Twitter and the dialogue that these, and other similar tools, enable. Social media appeared to impact publications in three areas: content distribution and promotion; online referrals to publications’ digital content and; tools to allow readers’ involvement in a story through rating buttons and comment features. There were numerous references to desktop usage in traditional markets “beginning to plateau” and, consequently, alternative ways of promoting and marketing content become more appealing. As Folwell says, “[The Guardian is] investing more in distributing our journalism and allowing people to connect with it off our platform, via social media” (34).

Increasingly, journalists are not working alone. They are no longer the sole creators of content for stories; instead, readers are recommending information for use in stories and promoting journalistic content through their social networks on social media like Twitter, Facebook and Digg. Emily Bell, Director of Tow Center for Digital Journalism at Columbia University, says that in a traditional newspaper environment “all the processes leading up to the delivery of that set of stories, on a daily or weekly basis, is very much set up to deliver finality [and is] built around a competitive landscape where you protect your story until its published. Digital media is not like that.” The trend of social media affecting consumer’s relationship to news is supported by data from the Pew Research Center’s Internet and American Life Project, which states that, “37 percent of Internet users have contributed to the creation of news, commented about it, or disseminated it via postings on social media sites like Facebook or Twitter” (35). As such, interviewees discussed grappling with a new world dominated by more participatory news consumer where, according to Ed Roussel, Director of Online for The Telegraph, “readers expect to take active part in the story, to respond to it and contribute to it.” There was a consistent sense from the participants that engaging with readers resulted in higher quality of content including, as Roussel says, “getting your readers to take a look at a set of data and send in and publish their own thoughts about what the data represents.”

Not only is content being disseminated through social media, but readers are also being referred to publications’ digital content by social media. An increasing trend, seen recently with predominantly online publications, but likely to move to traditional publications, is a significant increase in traffic as a result of Facebook’s “Like” buttons and referrals. A “Like” button allows users to efficiently endorse and promote an article or piece of content to their social network. Although it is solely an online publication, a recent post on the political blog Talking Points Memo emphasized the importance of social media directing traffic to websites, “[…] the break-out growth also tracks pretty closely to when we (TPM) set up a “fan” page on Facebook, that now has over 34,000 fans, and began more systematically incorporating Facebook sharing tools into our basic story template.”

Organizational change

All participants discussed the challenges faced from an organizational perspective, when the relationship between technology and journalism is changing and developing so quickly. For Folwell, from the Guardian Media Group, “The primary challenge for an organization like ours is not so much that you don’t have enough money, because we do, it’s not that you’ve not got great people, because we do, it’s not that we haven’t got a brilliant brand. It’s that actually moving from A to B, when you don’t know where B is, is tricky, and moving with conviction is difficult.”

It is clear that as online becomes more important, organizations have to balance a change in resource allocation and investment from traditional print editorial to a more integrated system of content creation. “You have to have this dual personality of being a print person and also being an online person,” says the Irish Times’ Liam Kavvanagh. In terms of monetization, this throws up significant challenges as to where publications allocate resources. Carlos Fernando Monteiro Lindenberg Neto, General Director of Rede Gazeta in Brazil, says the group’s newspaper, A Gazeta, is working “towards the systematic charging of content distributed online and preparing the newsroom to work on more attractive content to make monetizing tablets more feasible.” It would appear that publications are starting to approach the dual (online and print) nature of distribution of content as an opportunity more than a threat, and are seeking a reinforcement between their online and print presence.

As content is increasingly delivered online, this transition has shaken up the traditional competitive structures of newspapers. For example, Folwell says that when evaluating a company’s online reach, “part of the complexity is that you begin competing against people that are not traditional competitors.” A number of our interviewees emphasized the change in mindset that this required causing them to begin to not “think in print terms anymore” (36). An important point to note is that this shift in focus is not occurring at the same time, the same rate or in the same way in different parts of the world. In Greece for example, one interviewee described the online market as “disorganized,” indicating that unlike in countries including the US and UK, the Greek online market was less developed. It was also common to find publishers and editors that felt the changes caused in the industry by the Internet were overstated (37). Dr. Berthold Hamelmann, Chief Editor of Germany’s Neue Osnabrücker Zeitung, argued that despite the importance of the development of the Internet, “[i]t is only important to earn enough money to pay for good and independent journalism. It doesn’t matter how it is distributed.”

The Irish Times sees the fact that it is now “competing in the English speaking world with the BBC, The Guardian, The New York Times and [that] there’s a massive appetite for news and information” as a particular challenge. It used to be that newspapers were clear about who their competitors were. It was not uncommon for price wars to occur between rival publications, such was the premium placed on being the paper that people instinctively picked up from the newsstand. Liam Kavvanagh, Managing Director, spoke about the changes in the industry, and when compounded with the financial crisis, providing an opening that did not exist before for innovation and thinking in this area; “It’s forcing people to rethink what they’re doing and maybe accelerating some of the trends that were there recently and hence that kind of pressure on us to find solutions in the online revenue question.”

Move to mobile

An area where our interviewees consistently saw significant growth potential in the future was in the use of mobile devices. Generally, when industry analysts discuss “mobile” they are talking about smartphones, for example the Android and iPhone, or tablet devices, the most ubiquitous of which is certainly the iPad. Although the period of rapid growth of audience for web based newspapers accessed via a desktop computer is not entirely over, one participant noted that “the very fast growth spurt we’ve had in recent years is beginning to tail off” and “the new growth will come from mobile”(38). As new platforms, specifically tablets, mobile and IPTV, become more prevalent the challenge to the structure of newspapers is to produce content and products that reflects the changing nature of consumption.

This involves a change in culture and a change in infrastructure. Across all publications journalists are being asked “to think about how stories will be represented on mobile and on our website, and you are asking people to do this at a time when they’re already under significant pressures, day to day”39. But also these changes are leading to a greater emphasis on multi media, which means that the process of putting together a story involves more components, leading to a more integrated newsroom. The most clearly defined example of this is at The Telegraph where a “content hub” is being developed, which is a tool that provides an interface that will “access both our content management system for digital and for the newspaper – we have two different systems – and allow journalists and editors to access a depth of content and put in relevant articles, stories, pictures and videos far more readily than they can now” (40).

As noted above, countries with a similarly underdeveloped online market, like Greece, are moving into creating content for mobile devices at a slower rate but see the potential in the future. “The mobile market hasn’t really advanced yet, but it is a great investment for more advertising revenues”(41).

The Future of Print Media – REGIONAL AND COUNTRY VARIATIONS

“National media systems are developing very differently as legacy media face comparable cyclical, technological and long-term challenges” (42). Throughout our research we understood that the notions of “crisis” for the business of journalism and “death of print media” are viewed differently across and within regions of the world. In fact, David A. Levy and Rasmus K. Nielsen say the crisis faced by the United States media system, “arguably the greatest crisis in recent history,” is more of an outlier among established industrial democracies43. While the American and many other Western news markets face challenges as a consequence of the media’s “twin crises,” emerging markets, such as India, Brazil and Chile, are experiencing growths in newspaper circulation and advertising revenues.

Recent data shows the “death of print” is, if even real, a limited phenomenon (44). Newspaper circulation declined 9.2 percent in North America and 2.9 percent in Europe between 2004 and 2009. By contrast, it increased 16.4 percent in South America, 16.1 percent in Asia and 14.2 percent in Africa during the same period45. Global print newspaper circulation declined 0.8 percent from 2008 to 2009, but overall circulation was 5.7 higher in 2010 than five years earlier46. By the end of 2010, revenues were expected to rise globally, according to data from the Pew Research Center’s Project for Excellence in Journalism.

Undeniably, the business of journalism is changing; but while in some cases it is shrinking, it is by no means disappearing (47). The news industry is being transformed, albeit at different speeds, with the rise of new tools (tablets and mobile phones), sources (social media) and audiences (rising middle- and low-income classes). As discussed in previous sections, media organizations have responded to economic, political and social pressures, complex challenges and emerging opportunities in a variety of different ways.

However one thing seems certain: the print newspaper crisis is not universal. As we seen throughout this study, readers are accessing news through different media platforms, ranging from print, radio and television to Internet and mobile applications. However the majority of professionally produced news journalism is, in most countries, still primarily underwritten by what Levy and Nielsen call “multi-media news organizations with a particular emphasis on print”(48). We have identified common underlying cyclical, technological and long-term challenges facing news organizations worldwide. Companies face a cyclical downturn in advertising as a result of the global financial crisis of 2007-849. They also face increased competition for audience attention and advertising revenues, and a new media environment with the rise of new technologies, including cable and satellite television and the Internet (50).

Finally, news organizations also face challenges stemming from political (market regulation and liberalization), social (fragmented news environment and volatiles audiences) and economic (changing business models) developments. However even with these similarities, differences in audience demand, market structure and media regulation point to different present and future scenarios for media markets (51). While the American and other Western newspaper markets suffer declines in readership and revenue, economies within the developing world are seeing their news industry grow in all platforms, including print. In countries like the United States, Greece and the United Kingdom, the business of journalism is suffering from cost-cutting measures, reduced consumption, declining resources, consolidation and its accompanying challenges (52). In other markets, including Brazil and India, newspapers are seeing an average increase in consumption, resources and competition. Chile boasts the largest growth in newspaper circulation of all OECD countries (53), with approximately 60 newspapers for 1000 readers.

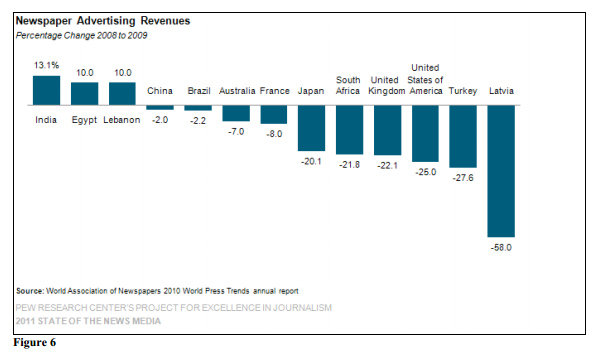

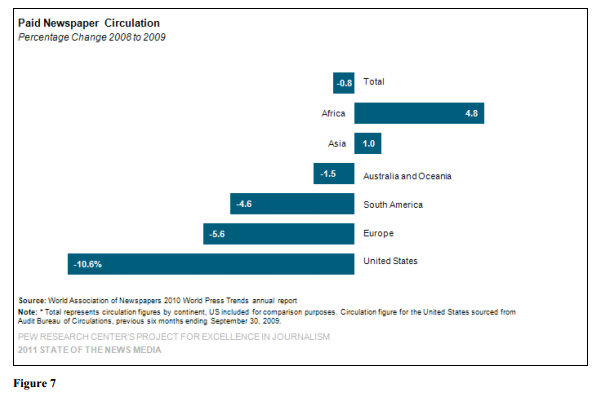

Markets where print newspapers are more dependent on revenues from advertising were more severely affected by the economic recession. Worldwide, advertising comprises 57 percent of overall newspaper revenues while circulation makes up 43 percent (54). In the United States, newspapers generate on average 73 of revenues from advertising, and sell their print copies at lower prices. In Germany newspapers generate 53 percent of their revenues from advertising (55). In the United Kingdom the average is 50 percent. From 2008 to 2009, newspapers’ advertising revenues declined 25 percent in the United States, 22.1 percent in the United Kingdom and 2.2 percent in Brazil. By contrast, they increased by 10 percent in Egypt and Lebanon, and by more than 13 percent in India (56). Newspaper circulation fell by 10.6 percent in the United States, 5.6 percent in Europe and 4.6 percent in South America; and grew by 1 percent in Asia and 4.8 percent in Africa from 2008 to 2009 (57). Figure 6 presents data on the percentage change of newspaper advertising revenues from 2008 to 2009. Figure 7 presents numbers on the percentage change in paid newspaper circulation for the same period.

As repeatedly stated throughout our interviews, the impact of the global financial crisis and subsequent recession was different for media organizations throughout the world. From 2007 to 2009 revenue change in newspaper publishing, including advertisement, sales and other sources of income decreased 30 percent in the United States, 21 percent in the United Kingdom, 20 percent in Greece and 10 percent in Germany. By contrast it grew by 9 percent in India (58). The year-on-year change for total advertising expenditures from 2007 to 2008 was (-)10.4 percent in the United Kingdom, (-)6.3 percent in the United States, 6.8 percent in Germany, 19.3 percent in India and 20.3 percent in Brazil (59).

Today print newspapers in many developing markets, including India and Brazil, are thriving, in part because of rising literacy, employment, education and income levels. Overall circulation in 2009 rose by 4.8 percent in Africa and 1.03 percent in Asia – the latter is home to 67 of the 100 largest newspapers in the world (60). South America enjoyed a 1.8 percent increase in circulation in 2008, followed by a 4.6 percent decline in 2009 (61). Literacy rates in North America and Europe are at 95 percent, a stable percentage for most of the past decades. By contrast, in Asia, the average literacy rate rose from 69.8 percent (1985 to 1994) to 81.5 percent (2005 to 2008), according to data from the United Nations Educational, Scientific and Cultural Organization. During the same periods, in Africa, the literacy levels among adults increased from 52.1 percent to 63.4 percent. Rising literacy rates are usually accompanied by increases in disposable income, which in turn create potential new newspaper audiences. Even within these regions, closer country analyses reveal complexities of the global newspaper industry. In Japan, newspaper daily reach was at 92 percent of the adult population in 2008. In 2010, 90 percent of Japanese claimed their preferred form of media was a newspaper (62). However industry net profit fell by 91 percent in 2008 after decreasing by 33 percent in 2007 (63). In neighboring Republic of Korea, where the number of online newspaper editions grew nearly 500 percent between 2005 and 2009, print circulation fell by only 2 percent during the same period (64). More than 77 percent of South Koreans say they prefer getting their news online, compared with 51.5 percent who prefer print newspapers (65). In China, overall newspaper circulation increased by more than 10 percent for paid newspapers between 2005 and 2009 and revenues from advertising rose by 6.4 percent in 2008 (66).

India provides an interesting example, where the number of dailies (excluding free papers) rose by nearly 45 percent and circulation rose by 40 percent from 2008 to 2009(67). Expenditures on advertising increased almost 19 percent in 2008 and 4.5 percent in 2009 (68). The literacy rate in the country rose from around 33 percent of the population in 1976 to 82 percent in 2009 (69). However even this thriving market faces challenges; the percentage of adults who read the newspaper every day is decreasing while the percentage of casual or occasional readers increases (70).

At the other extreme, the United States publishing market shrunk more dramatically in recent years than in most of the world. American newspapers suffered a near 30 percent drop in revenues from online and offline circulation and advertising from 2007 to 2009 (71). This decline was particularly significant because advertising sales comprise nearly three quarters of American newspaper revenues. By contrast, in Europe, newspaper sales account for around 50-60 percent of all revenue, and advertising makes up the remaining 40-50 percent of revenue (72). In England, overall circulation dropped 7 percent among paid-for daily newspapers. The country’s ten national newspapers suffered a near 20 percent drop in copy sales from 2000 to 2009, according to the Audit Bureau of Circulations (ABC)(73). Print revenues from advertising fell 17 percent in 2009, continuing a fiveyear decline of nearly 30 percent (74). In general, European newspapers are not suffering as severely as American publications (75). From 2007 to 2009 newspaper revenues fell by 21 percent in the United Kingdom, 20 percent in Greece and 10 percent in Germany (76). European print publications depend less on revenues from advertising than their American counterparts; many are family-owned and relied heavily on private money during the financial crisis and following recession.

In addition, Northern European countries have historically higher rates of newspaper readership than the United States (77). In the US, newspapers had a daily reach of 45 percent for daily copies and 48 percent for Sunday editions, in 2008, compared with a 55 percent reach in 2001 (78). By contrast, some European countries enjoyed increases in the percentage of adults who claim to regularly read a daily newspaper, compared with previous years, like Switzerland (80 percent) and Ireland (58 percent)(79). The distribution of advertising expenditures also differs from country to country. For instance, Germany, the United Kingdom and the United States have similar levels of broadband penetration, with fundamentally different distributions of advertising revenues. Internet sites attract 15 percent of all advertising expenditures in Germany and the United States, 23 percent in the United Kingdom and almost zero in Brazil. Newspapers attract 37 percent of all advertising expenditures in Germany, 29 percent in Brazil, 28 percent in the United Kingdom and 22 percent in the United States (80).

Newspapers around the world are being hit by all the same trends now visible in the United States market, “but they are about 7 to 10 years behind,” says media economist Robert Picard (81). The view in most publications is not that they are immune to the “problems of American newspapers,” but rather that the American industry is ahead of them in navigating a dangerous curve. While publications in economies like Brazil and Chile are not suffering from the immediate loss of advertising and readership experienced by many Western newspapers, and hold a generally optimistic view for the future of print, they can see their audiences moving online. News markets in Asia, Africa and South America may not have matured fully yet, but they should expect to be faced with similar challenges in the next 10 to 20 years.

The Future of Print Media – CONCLUSION

This paper has sought to interrogate the commonly held assumption by media analysts and commentators that the newspaper industry is in perpetual decline. To be sure, the idea of the “death of print” is founded in a realistic assessment of the impact of technological advances. But the shift away from the traditional business model of the printing press is not new, it has been occurring since the early 1980s. Perhaps the most graphic depiction of the changes caused by new technologies in the last forty years has not been the recent advent of Apple’s iPhone applications or The New York Times paywall. But instead the riots that took place in 1986 when Rupert Murdoch shut down the printing presses in Wapping, London and moved his News International titles to Canary Wharf in the Dockands. Buoyed by a resurgence of the free market and an anti-union backlash, this period marked the beginning of the end for the traditional business model of newspapers. However it is also fair to say that in recent years this decline has been perpetuated by the onset of the Internet and the 2007-8 financial crisis, or what we have called the “twin crises.”

The health of the newspaper industry, how newspapers are being discussed and what people consider the “state of the industry,” is an important area of research. Although it seems an obvious assertion, a robust and free media is a fundamentally important part of a representative democracy. The policy implications of restricting newspapers’ ability to hold governments accountable is quite simply governance by oppression. The maintenance of a free “market place of ideas,” where discussion and debate can flourish is a cornerstone of any democratic society.

In the course of our research, which has included a literature review, contributions from experts, authors and academics and over 24 interviews with directors and editors from around the world, it has become clear that “crisis” and “death” are two very strong words. While we appreciate there are considerable limitations to a methodology that asks business owners to publicly declare whether the organizations they run are in good shape, 43 we have also been surprised by the frank and honest conversations we have had with those working on the frontline of journalism and newspaper publishing.

Our key findings have been centered on publications seeking alternative revenue streams to make up for lost revenue from print advertising sales. We have found that many publications have been stretching the trusted brands they have created to capitalize on brand loyalty and move into commerce; selling wine, vacations and even dating services.

Diversification of non-media holdings and investments have also been a response to the challenging financial environment. A desire to establish a model that is able to take make money from producing content online has been a common theme throughout our discussions. It is clear that whether or not they are being affected by audiences moving online to gather their news at the moment, almost all those interviewed saw this as the key challenge facing the industry. It is also important to note that in many emerging economies, there is considerable variation away from the “declining print” model. In fact, in many countries, including Brazil, India, and even Switzerland and Greece, print is said to be thriving.

A key aspect of this research has been to clarify that blanket assertions about the state of the industry, stemming mostly from an American and Western European perspective, are simply not accurate. Both in terms of the optimism and engagement with the process of change encountered in discussions with representatives of those markets, but also with those who’s opinion is perhaps less often canvassed. It is clear that the newspaper industry is not in the process of marching towards its death, but is coming to terms with a period of uncertainty and rapid technological change. The challenge of the future, while it is uncertain, is one that the industry appears to be increasingly ready to meet. In the words of Eugen A. Russ, Managing Director of Germany’s Voralberger Medienhaus, “Newspapers won’t be dead in the future […], the newspaper industry faced several technological disruptions, like TV, already, but it always found a way to survive.”

The Future of Print Media – APPENDICES

List of Interviewees by Country

Brazil (interviews by Samantha Barthelemy)

Silvio José Genesini Júnior, Chief Executive Officer of Grupo Estado

Carlos Fernando Monteiro Lindenberg Neto, General Director of Rede Gazeta

Marcelo Rech, General Director for Product for Grupo RBS

Chile (interview by Adrienne Jarsvall)

Juan Jaime Diaz, Deputy Director of El Mercurio

Germany (interviews by Tim Christiansen)

Berthold Hamelmann, Chief Editor of Neue Osnabrücker Zeitung

Christoph Keese, President of Public Affairs, Axel Springer AG

Eugen A. Russ, Managing Director of Voralberger Medienhaus

Tobias Trevisan, Managing Director of Frankfurter Allgemeine Zeitung

Greece (interviews by Katerina Koinis)

Theocharis Filippopoulos, Publisher, President & CEO of Attica Publications Group

Thodoris Georgakopoulos, Chief Internet Officer and Senior Editor, IMAKO

George Kalofolias, Publisher & CEO of Express Kalofolias Group

Ioannis Liotos, Commercial Director, Naftemporiki

Yannis Perlepes, General Manager, Naftemporiki

Switzerland (interviews by Adrienne Jarsvall)

Markus Spillmann, Editor in Chief of Neue Zuercher Zeitung

Christoph Zimmer, Head of Communications, Tamedia

United Kingdom

Emily Bell, Director of Tow Center for Digital Journalism at Columbia University

Steve Folwell, Head of Strategy, Guardian Media Group

Liam Kavvanagh, Managing Director, Irish Times

Ed Roussel, Director of Online, The Telegraph

The Future of Print Media – REFERENCES

(1) Levy, David, Changing Business of Journalism and its Implications for Democracy, Reuters Institute for the Study of Journalism, 2010, p. 1175

(2) Snyder, J and Ballentine, K, Nationalism and The Marketplace for Ideas, International Security, 1996, p. 12.11

(3) The Evolution of News and the Internet, Committee for Information, Computer and Communications Policy, OECD 2010, p. 7.

(4) World Press Trends: Advertising Revenues to Increase, Circulation Relatively Stable, World Association of Newspapers 2010, http://www.wan-press.org/article18612.html12

(5) World Press Trends Report, World Association of Newspapers 2010, http://www.wan-ifra.org/13

(6) World Press Trends: Advertising Revenues to Increase, Circulation Relatively Stable,World Association of Newspapers 2010, http://www.wan press.org/article18612.html14

(7) Karp, Scott, Newspaper Online vs. Print Ad Revenue: The 10% problem, 2007, Publishing 2.0, http://publishing2.com/2007/07/17/newspaper online-vs-print-ad-revenue-the-10-problem/

(8) Levy, David, Changing Business of Journalism and its Implications for Democracy, Reuters Institute for the Study of Journalism, 2010, p. 118.

(9) World Press Trends: Advertising Revenues to Increase, Circulation Relatively Stable, World Association of Newspapers 2010, http://www.wan- press.org/article18612.html

(10) World Press Trends: Advertising Revenues to Increase, Circulation Relatively Stable, World Association of Newspapers 2010, http://www.wan-press.org/article18612.html

(11) Levy, David, Changing Business of Journalism and its Implications for Democracy, Reuters Institute for the Study of Journalism, 2010.

(12) Interview with Thodoris Georgakopoulos, Chief Internet Officer of IMAKO Group, Greece, 2011.

(13) For more information, see the “Revenue Alternatives” Section.

(14) Interview with Marcelo Rech, General Director for Product, Grupo RBS, Brazil, 2011.

(15) Broniarczyk, Susan M. & Alba, Joseph W., The Importance of the Brand in Brand Extension, Journal of Marketing Research, 1994, p. 215.19

(16) Interview with Carlos Fernando Monteiro Lindenberg Neto, General Director, Rede Gazeta, Brazil, 2011. 20

(17) Plunkett Research 2010, Introduction to the Advertising and Branding Industry http://www.plunkettresearch.com/advertising%20branding%20market%20research/industry%20overview

(18) IDATE Consulting and Research, Telecoms, Internet, Media 2009 http://www.idate.org/en/Digiworld/DigiWorld-Yearbook/2009-s-edition/2009-s-edition_43_.html22

(19) Interview with Eugen A. Russ, Managing Director of Voralberger Medienhaus, Germany, 2011.

(20) Interview with Dr. Berthold Hamelmann, Chief Editor of Neue Osnabrücker Zeitung, Germany, 2011.

(21) Interview with Thodoris Georgakopoulos, Chief Internet Officer of IMAKO Group, Greece, 2011.

(22) Interview with Dr. Berthold Hamelmann, Chief Editor of Neue Osnabrücker Zeitung, Germany, 2011.

(23) Plunkett Research 2010, Introduction to the Advertising and Branding Industry http://www.plunkettresearch.com/advertising%20branding%20market%20research/industry%20overview

(24) IDATE Consulting and Research, Telecoms, Internet, Media 2009 http://www.idate.org/en/Digiworld/DigiWorld-Yearbook/2009-s-edition/2009-s-edition_43_.html

(25) Levy, David, Changing Business of Journalism and its Implications for Democracy, Reuters Institute for the Study of Journalism, 2010.

(26) Interview with Christoph Keese, President of Public Affairs, Axel Springer AG, Germany, 2011.

(27) Internet Advertising Revenue Report. Herausgegeben von Interactive Advertising Bureau, PricewaterhouseCoopers, 2011, p. 20.

(28) Indian Media and Entertainment Outlook 2010, PricewaterhouseCoopers, Delhi, p. 20.

(29) Plunkett Research 2010, Introduction to the Advertising and Branding Industry http://www.plunkettresearch.com/advertising%20branding%20market%20research/industry%20overview 30 Ibid.

(31) Benton, J, Nieman Journalism Lab, Harvard University, March 21st 2011, http://www.niemanlab.org

(32) Interview with Steve Folwell, Head of Strategy, Guardian Media Group, United Kingdom, 2011.

(33) Kaplan, Andreas M.; Michael Haenlein, Users of the World, Unite! The Challenges and Opportunities of Social Media, Business Horizons 53 (1), 2010, p. 59–68

(34) Interview with Steve Folwell, Head of Strategy, Guardian Media Group, United Kingdom, 2011.

(35) Purcell, Kristen, Understanding the Participatory News Consumption, 2010, http://www.pewinternet.org/Reports/2010/Online-News.aspx

(36) Interview with Dr. Berthold Hamelmann, Chief Editor of Neue Osnabrücker Zeitung, Germany, 2011.

(37) Interview with Ioannis Liotos, Commercial Director of Naftemporiki, Greece, 2011.

(38) Interview with Ed Roussel, Director of Online, The Telegraph, United Kingdom, 2011.

(39) Interview with Liam Kavvanagh, Managing Director, Irish Times, United Kingdom, 2011.

(40) Interview with Ed Roussel, Director of Online, The Telegraph, United Kingdom, 2011.

(41) Interview with Ioannis Liotos, Commercial Director of Naftemporiki, Greece, 2011.

(42) Levy, David, Changing business of journalism and its implications for democracy, Reuters Institute for the Study of Journalism, 2010, p. 2.

(43) Ibid, p. 95, 135.

(44) Ibid, p. 117.

(45) Shaping the Future of the Newspaper 2009, World Association of Newspapers, p. 2.

(46) State of the News Media Report, 2011, http://stateofthemedia.org/

(47) Ibid, p. 1, 4.35

(48) Levy, David, Changing business of journalism and its implications for democracy, Reuters Institute for the Study of Journalism, 2010, p. 3

(49) Ibid, p. 4.

(50) Ibid, p. 4.

(51) Ibid, p. 1, 4.

(52) Ibid, p. 17

(53) OECD, Media Trends Survey.

(54) The Evolution of News and the Internet, Committee for Information, Computer and Communications Policy, OECD 2010.

(55) Levy, David, Changing Business of Journalism and its Implications for Democracy, Reuters Institute for the Study of Journalism, 2010.

(56) State of the News Media Report, 2011, http://stateofthemedia.org/

(57) Ibid.

(58) The Evolution of News and the Internet, Committee for Information, Computer and Communications Policy, OECD 2010 and PricewaterhouseCoopers 2010.

(59) World Advertising Research Centre, WARC, 2010.

(60) State of the News Media Report, 2011, http://stateofthemedia.org/

(61) World News Future & Change Study 2010, World Association of Newspapers 2010.

(62) State of the News Media Report, 2011, http://stateofthemedia.org/

(63) State of the News Media Report, 2011, http://stateofthemedia.org/

(64) Ibid.

(65) The Evolution of News and the Internet, Committee for Information, Computer and Communications Policy, OECD 2010.

(66) Shaping the Future of the Newspaper 2009 and World News Future & Change Study 2010, World Association of Newspapers.

(67) State of the News Media Report, 2011, http://stateofthemedia.org/

(68) Ibid.

(69) World News Future & Change Study 2010, World Association of Newspapers 2010.

(70) State of the News Media Report, 2011, http://stateofthemedia.org/

(71) Ibid.

(72) Ibid.

(73) World News Future & Change Study 2010, World Association of Newspapers 2010.

(74) State of the News Media Report, 2011, http://stateofthemedia.org/

(75) Ibid.

(76) The Evolution of News and the Internet, Committee for Information, Computer and Communications Policy, OECD 2010.

(77) State of the News Media Report, 2011, http://stateofthemedia.org/

(78) The Evolution of News and the Internet, Committee for Information, Computer and Communications Policy, OECD 2010

(79) State of the News Media Report, 2011,

(80)International Communications Markets 2009, Ofcom, London and World Advertising Research Centre, WARC, 2008.

(81) International Communications Markets 2009, Ofcom, London and World Advertising Research Centre, WARC, 2008.

The Future of Print Media – BIBLIOGRAPHY

Ahlers, Douglas News Consumption and the New Electronic Media (2006) The International Journal of Press and Politics

Benton, J, The Nieman Journalism Lab at Harvard University, March 21st 2011 http://www.niemanlab.org

Broniarczyk, Susan M.; Alba, Joseph W. The Importance of the Brand in Brand extension (1994) Journal of Marketing Research

Chua, Reg (Re)Structuring Journalism; Rethinking Journalism and the Business of Journalism From the Ground up (Blog) http://structureofnews.wordpress.com/

Cudlipp, Hug Does Journalism Exist? (2010) Lecture Committee for Information, Computer and Communications Policy, The Evolution of News and the Internet, OECD (2010)

The Economist The Crucible of Print (2011) http://www.economist.com/node/17853358

George, Lisa M. and Waldfogel, Joel The New York Times and the Market for Local Newspapers, (2006) The American Economic Review, Volume 96, Number 1

George, Lisa and Waldfogel, Joel Who Affects Whom in Daily Newspaper Markets? (2003) Journal of Political Economy

Haas, Tanni The Pursuit of Public Journalism; Theory, Practice and Criticism (2007) Routledge

Herausgegeben von Interactive Advertising Bureau, Internet Advertising Revenue Report, (2011), PricewaterhouseCoopers

Hsiang, Iris Chyi Willingness to Pay for Online News: An Empirical Study on the Viability of the Subscription Model (2005) Journal of Media Economics

IDATE Consulting and Research, Telecoms, Internet, Media 2009 http://www.idate.org/en/Digiworld/DigiWorld-Yearbook/2009-s-edition/2009-sedition_43_.html

Interactive Advertising Bureau, Internet Advertising Revenue Report (2011), http://www.iab.net/

Kaplan, Andreas M. and Haenlein, Michael Users of the world, unite! The challenges and opportunities of Social Media (2010) Business Horizons 53 (1)

Karp, Scott Newspaper Online vs. Print Ad Revenue: The 10%Problem (2007) Publishing 2.0

Knee, Peter; Greenwald, Bruce; Seave, Ava Curse of the Media Moguls (2009) Portfolio